With the onset of the Affordable Care Act (aka

Obamacare), enrolling in a health plan has been restricted to a particular time

frame called Open Enrollment. This generally

happens toward the end of the calendar year, with new plans beginning January 1st

of the following year. But what do you

do if something changes in your life and you need new health insurance

mid-year? You may or may not be able to

get it. Here are the 10 categories that

will afford you a Special Enrollment Period (SEP) in which to enroll in a new

health plan:

Losing other qualifying coverage:

You were on Medi-Cal and no longer qualify

If you newly qualify for Medi-Cal, you can enroll at any time.

You had employer-sponsored coverage and lost/quit your job

You had COBRA and exhausted those benefits. Dropping COBRA because it is too expensive DOES NOT qualify. However, you do not have to accept COBRA if it is offered to you.

You no longer qualify for a student health plan through a university

You turn 26 years old and need to come off your parent’s plan

You turn 19 and no longer qualify for a ‘child only’ plan

You no longer qualify for military coverage

Changes in household size

Marriage, divorce, legal separation

Birth or adoption of a child

Death

Any other situation where you lose a dependent or your status as a dependent

Changes in residence

Permanently moved from out of state

Permanently moved within the state to a location that offers at least one new Covered CA plan to which you previously did not have access

Permanently moved within the state and your current plan is not offered in your new location

Changes in eligibility for financial help

Gain or lose status with Medi-Cal

Lose your ‘share of cost’ with Medi-Cal by reaching your share of cost

Defined types of errors made by the Marketplace, Plans, or Agents

You were given misinformation during the enrollment process

There were technical errors with the software during your enrollment

There were errors in the processing of your eligibility determination

Release from jail or prison

Gained Citizenship or Lawful Presence

Member of a Federally recognized American Indian or Alaska Native tribe

Members have an open Special Enrollment Period and can enroll at any time

Members can change plans once every month

Your provider (doctor) left the plan’s network AND you have one of the following:

Pregnancy

Terminal Illness

Acute Condition

Serious Chronic Condition

Care of a child between the ages of 0 – 36 months

Surgery or Procedure scheduled within 180 days of the provider’s change

All Other Reasons

Natural disaster (fire, flood, hurricane, etc.)

You had a medical emergency that precluded you from enrolling during open enrollment

You are a victim of domestic violence or spousal abandonment

You have a court order to provide insurance for a dependent, even if you will not be claiming that dependent on your tax return.

It’s a long list to remember. So, if you just remember that the

circumstances must be beyond your control, you will probably find that you

qualify for a Special Enrollment Period.

But be mindful: your SEP is only

60 days long and starts the day your change happens. If you miss your 60-day window, you will have

to wait for the next Open Enrollment Period to receive a plan beginning the

next year.

Unfortunately, California no longer allows interim, or

short-term, plans to carry you through.

Your only options are the Marketplace (Covered CA) or purchasing

something directly with the insurance company.

A health insurance broker (like Pronoeo Insurance Agency) can guide you.

The intent seems to get lost in the translation. People use these words interchangeably, but they really mean different things. There are several proposals on the table in Congress that this article does not address. The two that seem to be gaining popularity are MEDICARE FOR ALL and SINGLE PAYER.

MEDICARE is government insurance alongside private insurance.

There are premiums that are paid by the insured for BOTH the Medicare coverage and the Private Insurance coverage. Typically, there are also deductibles and copays or coinsurance that are paid by the insured as well. There is no coverage for Long-Term Care, Vision, or Dental with Medicare. However, some private insurers have added the opportunity to purchase those services at an additional premium.

SINGLE PAYER is only government insurance.

They cover anything that is MEDICALLY NECESSARY, which may include some form of Long-Term Care, Vision and/or Dental. The insured does not pay any premiums, deductibles or copays. The entire program is funded with increased taxes to the general population. The government controls all aspects of medical distribution, to include payment of claims to doctors and medical facilities as well as access to medical technology. Costs are controlled by controlling/limiting access to services.

There are advantages and disadvantages to both:

MEDICARE FOR ALL would still allow your doctor to make medical decisions based on your needs as opposed to a governmental agency regulating your care. People would still have choices regarding their private insurance portion, which would maintain some sort of competition between insurance companies to vie for your business. Increasing the number of people on Medicare would be expensive. Our current Medicare system is not financially sound – adding the entire population to it would mean a large increase in taxes to pay for it.

SINGLE PAYER would lower some administrative costs, as well as some profits. But putting the entire medical bill on the government means putting it on the taxpayers. Studies have also found that, in a Single-Payer system, research and development of new technologies and medications goes out the window because there is no funding and no incentive for that market.

How Much Are You Willing To Pay?

In either situation, the cost of these programs is coming out of your pocket. People don’t seem to understand that the government has only one source of income: YOU. When you say, “let the government pay for it,” what you are really saying is “let the people pay for it.” The people are the only source of income for the government. For them to have money to pay for something, they must raise taxes.

In California alone, it is estimated that we would need to add over $418 Billion to our current $209 Billion state budget in order to begin to pay for healthcare, with the numbers anticipated to rise from there – rapidly. The numbers nationally are mind-boggling.

Conclusion

The US currently spends 2-3 times more per capita than any other country for medical care. Then again, we are on top for research and development. People from other countries come here to be treated because they can get relatively quick access to services and technology compared to what they have in their country.

I can’t help but be reminded of the Scripture in 1 Samuel 8:19 where the people of Israel cried out, “We want a king over us. Then we will be like all the other nations…” As it turned out, being “like all the other nations” didn’t work out too well for them. We will have to see how this healthcare situation flushes out and see if history really does repeat itself.

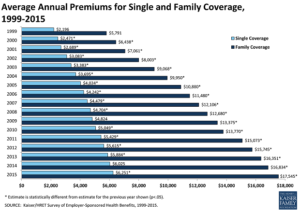

The cost of medical insurance in California (and nationwide) has spiraled out of control. It is not uncommon for a married couple to be paying more for medical insurance than for their mortgage. And then they can’t afford to use the insurance because of ridiculous deductibles and copays.

Factors:

Unfortunately, it’s a lot like homelessness: there is no ONE underlying cause. There are many factors that drive up the cost of healthcare:

Fee-for-Service systems: providers (doctors and facilities) are paid per procedure so it incentivizes them to utilize many procedures and tests, even if it isn’t warranted by the diagnosis. On the flip-side, underpayment or low reimbursement of these procedures also encourages over-treatment because the providers don’t make enough to cover their costs.

We have an aging population. Over 70% of the medical services you receive in your lifetime will be received in your retirement years. As we age, we become less resilient to disease and physical injury.

We want the latest drugs, technologies, services, and proceduresto keep us healthy. But new on the market usually equates to higher priced treatment.

Mergers and Acquisitionsof health organizations have created near monopolies in the various areas of medical care. When there is no one to compete against, you can set your prices wherever you want. M&A’s have caused the price of medical services to rise at a rate much higher than inflation.

We live in a litigious society. People know that doctors and hospitals have to carry malpractice insurance and see them as a ‘deep pocket.’ Doctors are afraid of being sued (sometimes ‘again’), and so there is a propensity to utilize defensive treatment: prescribing something “just in case” there may be a medical issue, so they won’t get sued.

With therate of reimbursement falling for Primary Care Physicians(your general/family doctor), there are more specialists in this country than there are Primary Care Physicians. Specialists are paid much more than a family doctor. Hence, we have a serious shortage of family physicians.

The cost of medications keeps going up – even the ones that have been on the market for years. This one, the politicians probably COULD fix. America is one of two countries worldwide that allow drug companies to advertise. We are paying for their advertising expense through our high drug prices. That’s why other countries don’t have a problem with high drug prices.

And I’m sure the list goes on and on. So let’s just PICK ONE, and fix it. Then we can work on the next one. Focusing on one problem at a time allows more resources to go to its solution instead of just doing a little here and a little there and so nothing gets completed. It’s just like eating an elephant – you can only do it one bite at a time. When the elephant has been consumed, everyone will have access to AFFORDABLE HEALTHCARE.

Healthcare has become such a political issue that the concept of “affordable healthcare” has vanished.

There is no single fix for obtaining affordable healthcare because the things making it unaffordable are as diverse as the people needing it. Let’s look at just three:

Current Issues:

1. Cost of care for CHRONIC DISEASES and overall POOR HEALTH.

The reality is that people with chronic diseases and/or overall poor health have greater medical needs and expenses than the average person. Medications, hospitals, ER and ambulance services are utilized more frequently by these individuals out of necessity, not because of system abuse. Finding a system that makes their care affordable is tricky – someone has to pay for all that.

2. Availability and access to DOCTORS and MEDICAL FACILITIES.

The current system may give more insurance coverage to individuals, but that does not equate to access to doctors and medical facilities. Reimbursements are so low, many doctors will not accept patients who are not part of an employer’s group policy. Many doctors have refused to accept Medicaid and Medicare patients because of the low reimbursements. The reality: it’s difficult to find a doctor, and when you do, you cannot get an appointment for weeks (or months).

3. QUALITY of available care.

Many of the providers that will accept the low reimbursements are rated poorly on sites on the internet. They may be fine providers under normal circumstances. But with low reimbursements, they are forced to push patients through as quickly as possible just so they can meet their overhead (rent, payroll, utilities, insurance, etc.). Misdiagnoses is the THIRD leading cause of death in the US (John Hopkins 2016). Doctors are forced to choose volume over quality.

MISCONCEPTION:

There is a misconception among our politicians that affordable health insurance equals affordable healthcare. There are two things wrong with that equation:

If you are not subsidized by a government program for your health insurance, it is ANYTHING but affordable. Especially if you are between 60-65 years old. Your monthly insurance premium could be more than your mortgage.

Deductibles, copays and coinsurance are so high on these insurance plans that people are avoiding going to the doctor when sick or injured.

Having access to insurance does NOT mean you have access to healthcare. Attempting to manage healthcare through the insurance industry is like relying on your auto mechanic for investment advice. And if you want to muck it up further, get a politician involved. YOU DON’T WANT SINGLE-PAYER.

Let’s work on actually addressing the causes of HEALTHCARE unaffordability and not INSURANCE affordability (a symptom). Coverage without access is an empty promise.

In Part 1, we looked at the changes in coverage and rating of the New Small Group. Part 2 discussed the penalties for employers that do not abide by the new ACA laws. In this article, we will discuss what an Applicable Large Employer (ALE) is and how that applies to the New Small Group. (more…)

Healthcare has become such a political issue that the concept of “affordable healthcare” has vanished.

Healthcare has become such a political issue that the concept of “affordable healthcare” has vanished. In Part 1, we looked at the changes in coverage and rating of the New Small Group. Part 2 discussed the penalties for employers that do not abide by the new ACA laws. In this article, we will discuss what an Applicable Large Employer (ALE) is and how that applies to the New Small Group.

In Part 1, we looked at the changes in coverage and rating of the New Small Group. Part 2 discussed the penalties for employers that do not abide by the new ACA laws. In this article, we will discuss what an Applicable Large Employer (ALE) is and how that applies to the New Small Group.